Does a 10% interest rate on your Crypto Dollars (Stablecoins) make sense?

Does a 10% interest rate on your Crypto Dollars (Stablecoins) make sense?

Breaking down the crypto dollar interest rate

When we stumble into crypto and look around, one of the first features we notice is the ability to earn 7-10% on our U.S. Dollars. Somehow, our checking account cash turns from crumbs to a bread maker. How can it be?

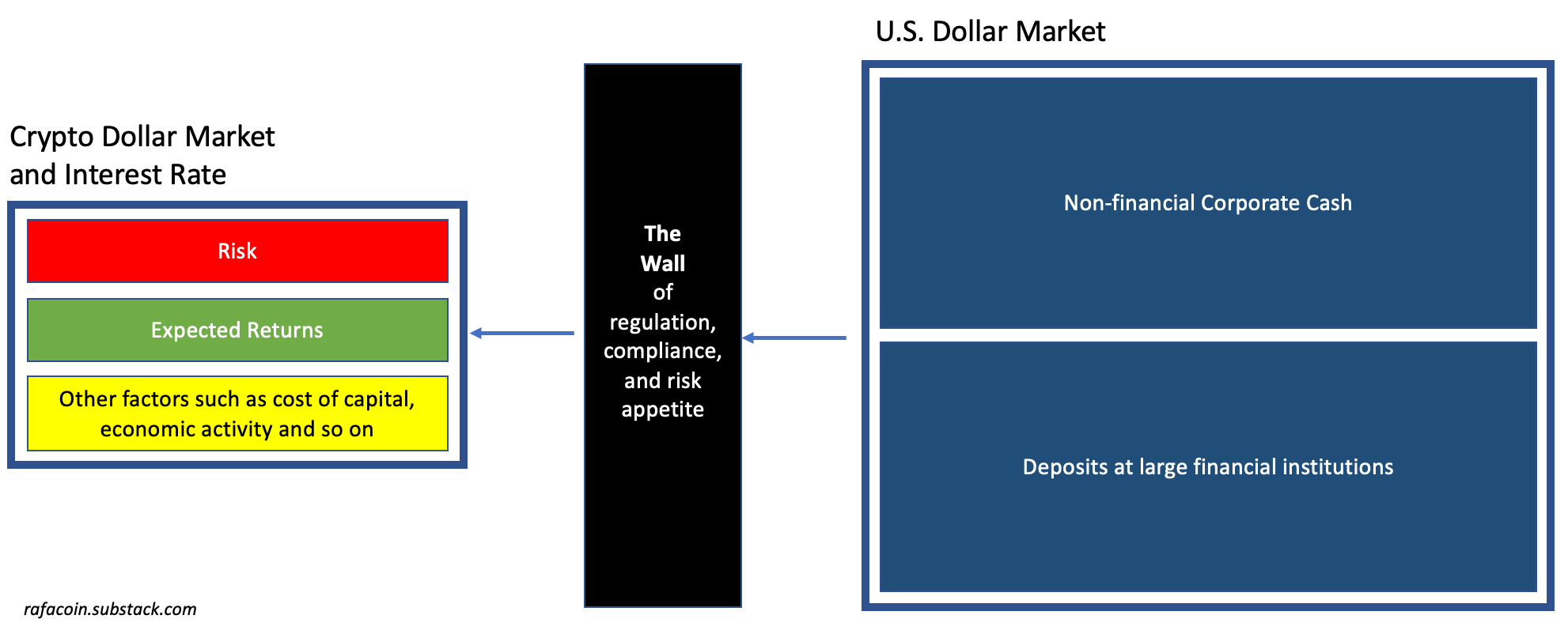

Off the bat, we'll hear that it's derived from the additional risk associated with the crypto dollar - also known as stablecoins. We're told that the crypto ecosystem is riskier, so that's the reason we get to earn more inside that system. It's true, but likely an incomplete statement. While risk is a component, expected returns along with supply and demand also play their role.

Let's break it down.

We'll start off with the risk conversation. There are definitely some factors that make our U.S. Dollars in the crypto ecosystem relatively riskier. Some examples include:

There's no FDIC insurance. However, remember that FDIC insurance is capped at $250,000. For any large institution or wealthy individual, this is not a significant threshold of protection

The dollars are tokenized by newer, unregulated, non-bank institutions such as Tether or Circle

The dollars are typically held (i.e. custodied) in locations that may carry additional hacking risk relative to traditional banks; and

Some portion of the dollars are lent to individuals, institutions and projects that are new and have no long-term track record of success

One could argue that through the invisible hand of Adam Smith, the market is just looking at such risks to reach the current interest rate levels. Stamp risk and 10% in the same piece of paper and we've solved the puzzle. Ted Lasso would say that's part of the Picasso, but there's more to it.

U.S. dollar rates in crypto were much higher not that long ago. The idea that a reduction in risk is what single handily reduced rates can't be the full picture. Credit risk is also not the only factor in an interest rate pricing equation.

In this conversation, loss risk is the lender’s view of the market. People with dollars choosing how much and where to lend their funds. On the other side though, we have the borrowers. The folks looking to deploy these dollars. If borrowing to make an investment, borrowers will consider expected returns.

Expected returns in crypto are currently higher relative to a lot of other asset classes. On the financial side, markets are fragmented and financial players can earn high rates of return employing simple arbitrage strategies and providing capital where there's scarcity. On the builder side, projects seem to have tremendous upside as new technology looks promising and is starting to grow in market share. A lot of people are willing to pay a good chunk of interest rate to get things done. Dollars are the grease to the wheel.

For the purpose of this article, we can simplify and assume that risk assessments along with cost of capital is what generally puts a floor on the interest rate level. It's the minimum return requirement for lenders. Meanwhile, expected returns push rates higher as borrowers are willing to pay up to get things done. One of the remaining large forces left to discuss is then supply and demand. Economics 101, back from the dead yet again.

Relative to demand, the amount of dollar supply in crypto becomes the question. The answer is that there isn’t enough dollars. It's funny to say that because there's definitely a lot U.S. dollars slushing around. When looking at companies in the S&P 500 (i.e. large cap US companies), they have $2.77 trillion in cash. The consensus complaint is that there's too much cash on the balance sheets!

If we then look to depository institutions, the top 5 US banks hold $7+ trillions in deposits.

As you might imagine, the vast majority of this cash is not available to crypto players. From regulatory and compliance to risk appetite reasons, many companies are not ready to deploy into the crypto ecosystem. Some players have made moves, but demand continues to outstrip supply.

If a large chunk of this cash was made available in the crypto ecosystem, we would likely expect U.S. dollar rates to drop significantly. Without the constraint of supply, we would probably see a more true risk-driven minimum rate of return. Here's another relevant supply situation to study.

When the Federal Reserve raised the benchmark Fed Funds rate from 2015 to 2018, you would have expected deposit rates for all of us to go up. It's how it usually happened in the past. However, this time around, banks had all our deposits - so plenty of supply - and they weren't interested in attracting more. As a result, rates on checking, savings and other short term deposits stayed close to zero while benchmark rates went up. Stablecoins weren't really around back then, so people looking to stay in cash while earning higher rewards didn't have many options.

Overall, the crypto dollar interest rate has multiple building blocks. It's an interplay of risk, expected returns, supply and demand, and other factors that we'll all continue to study in the next few years.

The cryptoverse can be emotional while places like Crypto Twitter can be simple and assertive. This is why, said with confidence. Fact is, we're all new here. I don't have the answer to it, and maybe, 10% does make sense.

In the future when we look back at historical returns and default rates, we'll have our answer. See you then.

All opinions here are my own. This is not investment advice.